Understanding how health insurance policy works can feel overwhelming, but it doesn’t have to be. This comprehensive guide breaks down the health insurance process from start to finish, explaining everything from what’s inside your policy document to how claims actually get processed.

What Does a Health Insurance Policy Contain?

When you purchase a health insurance policy, you’re essentially entering into a contract with an insurer. Here’s what that contract includes:

Sum Insured: Your Coverage Limit

The sum insured represents the maximum amount your insurer will pay for medical expenses during the policy year. For example, if you have a policy with ₹5 lakh sum insured, that’s your coverage ceiling for the year. Once exhausted, you’ll need to pay out-of-pocket unless you have a top-up plan.

The sum insured resets annually upon renewal, giving you fresh coverage each year. Some policies also offer a restoration benefit, which reinstates your sum insured if it gets exhausted during the year.

Network Hospitals: Where You Can Get Treated

Network hospitals are healthcare facilities that have agreements with your insurance company. These partnerships enable cashless treatment, meaning you don’t pay upfront for covered medical expenses. Most insurers in India have networks spanning 8,000 to 15,000 hospitals nationwide.

Always check your insurer’s network hospital list before seeking treatment. Going to a non-network hospital means you’ll need to pay first and file for reimbursement later.

Policy Inclusions: What’s Covered

Standard health insurance policies typically cover hospitalization expenses including room charges, doctor fees, surgery costs, medications, diagnostic tests, and ambulance charges. Many modern policies also include pre-hospitalization expenses for 30-60 days before admission and post-hospitalization costs for 60-90 days after discharge.

Advanced policies may include daycare procedures, AYUSH treatments, home healthcare, and even mental health coverage. The health insurance policy explained in your policy document will list all covered treatments and services.

Exclusions: What’s Not Covered

Policy exclusions are equally important to understand. Common exclusions include cosmetic procedures, dental treatments unless requiring hospitalization, infertility treatments, and expenses arising from self-inflicted injuries or substance abuse.

Pre-existing diseases are typically excluded for an initial waiting period. Specific illnesses like hernias, cataracts, and joint replacement surgeries may have waiting periods of 2-4 years.

Waiting Periods: The Timeline Factor

Health insurance policies have several types of waiting periods. The initial waiting period of 30 days applies to all illnesses except accidents. Pre-existing disease waiting periods range from 2-4 years depending on the condition and insurer. Specific disease waiting periods of 1-2 years apply to conditions like hernias, sinusitis, and stones.

Maternity coverage usually has a waiting period of 2-4 years. Understanding these timelines is crucial for planning your healthcare needs.

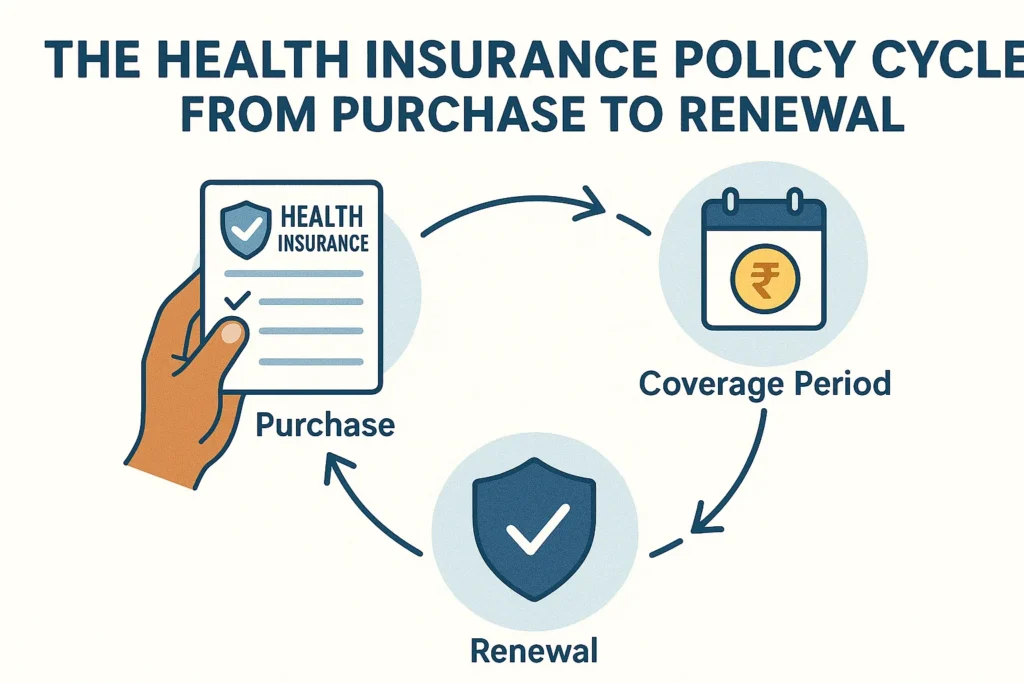

The Health Insurance Policy Cycle: From Purchase to Renewal

The health insurance process follows a predictable cycle that repeats annually:

Purchase Phase

You select a plan based on your needs, pay the premium, and receive your policy document within days. This document contains all terms, conditions, coverage details, and the policy schedule with your personal information.

Active Coverage Period

During the policy year, you can access medical care at network hospitals or seek reimbursement for treatments at non-network facilities. Your coverage remains active as long as premiums are paid.

Renewal Phase

Policies typically renew annually. Most insurers offer lifetime renewability, meaning you can continue coverage regardless of claims made or age. Premium adjustments may occur based on age, claims history, and medical inflation.

Claims Processing

When you require medical treatment, you’ll either use the cashless facility or file for reimbursement. Successful claims lead to payment of eligible expenses within your sum insured limit.

No-Claim Bonus Accrual

If you don’t make any claims during the policy year, many insurers reward you with a no-claim bonus, typically increasing your sum insured by 5-50% at the same premium or offering a discount on renewal premium.

Cashless Process Explained: How It Actually Works

The cashless treatment process is one of the most valuable features of how policy coverage works. Here’s the step-by-step breakdown:

Step 1: Hospital Admission and Pre-Authorization

When you need planned hospitalization, contact your insurer’s helpline or the hospital’s insurance desk 48-72 hours before admission. For emergency admissions, notify within 24 hours of hospitalization.

The hospital will help you fill out a pre-authorization form. You’ll need to provide your policy number, health card, identity proof, and doctor’s recommendation for treatment.

Step 2: TPA Verification and Processing

Your insurer works with a Third Party Administrator (TPA) who processes cashless claims. The TPA receives your pre-authorization request and verifies your policy status, coverage eligibility, and available sum insured.

The TPA reviews the proposed treatment against your policy terms, checking for exclusions, waiting periods, and sub-limits. This verification typically takes 2-6 hours for emergencies and up to 24 hours for planned procedures.

Step 3: Hospital Approval and Treatment

Once approved, the hospital receives authorization to proceed with treatment. You’ll typically only need to pay for non-covered expenses like room rent above your policy limit or consumables if not covered.

After treatment, the hospital submits final bills to the TPA. The insurer settles eligible expenses directly with the hospital. You’ll receive a discharge summary showing covered and non-covered expenses.

What If Pre-Authorization Is Denied?

If your cashless request is rejected, you can still proceed with treatment and file for reimbursement later. Denials typically occur due to exclusions, exhausted sum insured, policy lapse, or incomplete documentation. Always ask for the specific reason and verify if it’s correct.

Reimbursement Process: When You Pay First

The reimbursement process applies when you receive treatment at non-network hospitals or when cashless approval isn’t available.

Documents Required for Reimbursement

You’ll need to submit the completed claim form, original hospital bills and receipts, discharge summary, doctor’s prescriptions, diagnostic test reports, pharmacy bills, and payment proofs. For accident cases, include the FIR or medico-legal certificate.

Many insurers now accept digital submissions through mobile apps or email, making the process faster and more convenient.

Reimbursement Timeline

After submitting documents, insurers typically process reimbursement claims within 15-30 days. The insurer reviews medical records, verifies policy coverage, and calculates eligible expenses after applying deductibles, co-payments, and sub-limits.

If additional information is needed, the insurer will request it. Once approved, the claim amount is transferred to your bank account. You’ll receive a claim settlement letter explaining covered and non-covered expenses.

Key Differences from Cashless

In cashless treatment, you don’t pay upfront for covered expenses and approval happens before treatment. With reimbursement, you pay all expenses first and wait for repayment. Cashless is more convenient but limited to network hospitals, while reimbursement offers flexibility to choose any hospital.

Key Policy Features That Affect Your Coverage

Understanding these features helps you make the most of how health insurance policy works:

No-Claim Bonus (NCB)

NCB rewards claim-free years by increasing your sum insured without raising premiums. For example, a ₹5 lakh policy might grow to ₹7.5 lakh after three claim-free years with cumulative bonuses of 50%. Some policies offer premium discounts instead, reducing your renewal cost by 5-20%.

NCB is usually retained even if you switch insurers through portability, though terms vary by company.

Room Rent Limit

Many affordable policies have room rent restrictions, typically limiting coverage to 1-2% of sum insured per day. A ₹5 lakh policy with 1% room rent limit covers only ₹5,000 daily for room charges.

Here’s the catch: if you choose a room costing ₹10,000, insurers apply proportionate deduction to all expenses, not just room rent. With a 50% breach, all your treatment costs are reduced proportionately. Opting for policies without room rent limits or choosing appropriate room types prevents this issue.

Sub-Limits on Specific Treatments

Sub-limits cap coverage for certain treatments regardless of your total sum insured. Common sub-limits apply to cataract surgery (₹40,000-50,000 per eye), knee replacement (₹1.5-2 lakhs), hernia (₹50,000), and maternity (₹50,000-1 lakh).

These limits can leave you with significant out-of-pocket expenses even with adequate sum insured. Higher premium plans often eliminate or raise these sub-limits.

Co-Payment: Sharing the Cost

Co-payment requires you to pay a percentage of claim amount, typically 10-30%. A 20% co-payment on a ₹1 lakh claim means you pay ₹20,000 and the insurer pays ₹80,000.

Senior citizen policies often have mandatory co-payments. Some policies offer voluntary co-payment options that reduce premiums by 10-30%. Co-payment applies to every claim, so consider your ability to pay this recurring cost.

Deductible: The Amount You Pay First

A deductible is a fixed amount you pay before insurance coverage begins. With a ₹50,000 deductible, you pay the first ₹50,000 of any claim. If hospitalization costs ₹1.5 lakhs, you pay ₹50,000 and insurance covers ₹1 lakh.

Policies with deductibles have significantly lower premiums, making them suitable if you want coverage only for major hospitalizations and can afford minor expenses yourself.

Common Mistakes People Make with Health Insurance

Avoiding these errors can save you thousands when you need to use your policy:

Not Reading Exclusions Carefully

Many policyholders discover exclusions only when filing claims. Always read the exclusion list in your policy document. Pay special attention to disease-specific waiting periods, permanent exclusions like cosmetic surgery, and conditions related to your health history.

If you have pre-existing conditions, understand exactly when they’ll be covered and what documentation you’ll need at claim time.

Choosing Wrong Room Type During Hospitalization

This is perhaps the costliest mistake. Selecting a room that exceeds your policy’s room rent limit triggers proportionate deduction on all expenses, not just the room. A seemingly small room upgrade can reduce your entire claim by 30-50%.

Always check your policy’s room rent limit before admission and select a room within that limit. If you want flexibility, buy a policy without room rent restrictions.

Not Checking Network Hospital List

Assuming your preferred hospital is in the network can lead to reimbursement hassles when you need cashless treatment urgently. Before buying a policy, verify that major hospitals near your home and workplace are in the network.

Download your insurer’s hospital locator app and keep the network list updated. Networks change, so check annually during renewal.

Delaying Policy Purchase

Waiting periods mean you need to buy insurance before you need it. Buying at age 35 instead of 25 means waiting 2-4 years for pre-existing condition coverage. Buying after developing diabetes or hypertension may lead to permanent exclusions or rejection.

Premiums also increase with age. Starting early locks in lower rates and builds no-claim bonuses.

Not Disclosing Medical History

Non-disclosure of pre-existing conditions at the time of purchase can lead to claim rejection and policy cancellation. Insurers verify medical records during claims, and any mismatch with your proposal form gives them grounds to deny coverage.

Always disclose all pre-existing conditions, past treatments, and surgeries honestly. It’s better to pay slightly higher premiums than face claim rejection.

Ignoring Policy Document

Many people never read their policy wording, relying on marketing brochures or agent explanations. The policy document is your legal contract and the final authority on coverage. Brochures and verbal promises don’t matter if they’re not in the policy.

Spend an hour reading your policy document when you receive it. Note down coverage limits, exclusions, and claim procedures.

Making Your Health Insurance Work for You

Understanding how health insurance policy works transforms it from a confusing document into a valuable financial safety net. The key is selecting appropriate coverage based on your age, family health history, and financial situation.

Before hospitalization, always verify coverage with your insurer and choose network hospitals when possible. Keep all medical records organized and submit claims promptly with complete documentation. During renewal, review your coverage needs and consider upgrading sum insured or removing restrictive features like room rent limits.

Health insurance policy explained properly empowers you to make informed decisions, avoid costly mistakes, and ensure smooth claims when you need medical care. Take time to understand your policy thoroughly, and don’t hesitate to contact your insurer for clarification on any terms.

Need help with filing a claim? Check our detailed Claims Process Guide for step-by-step instructions. Wondering about premium calculations? Visit our Premium Calculator Page to estimate costs. For broader coverage information, explore our comprehensive Health Insurance Coverage Guide.